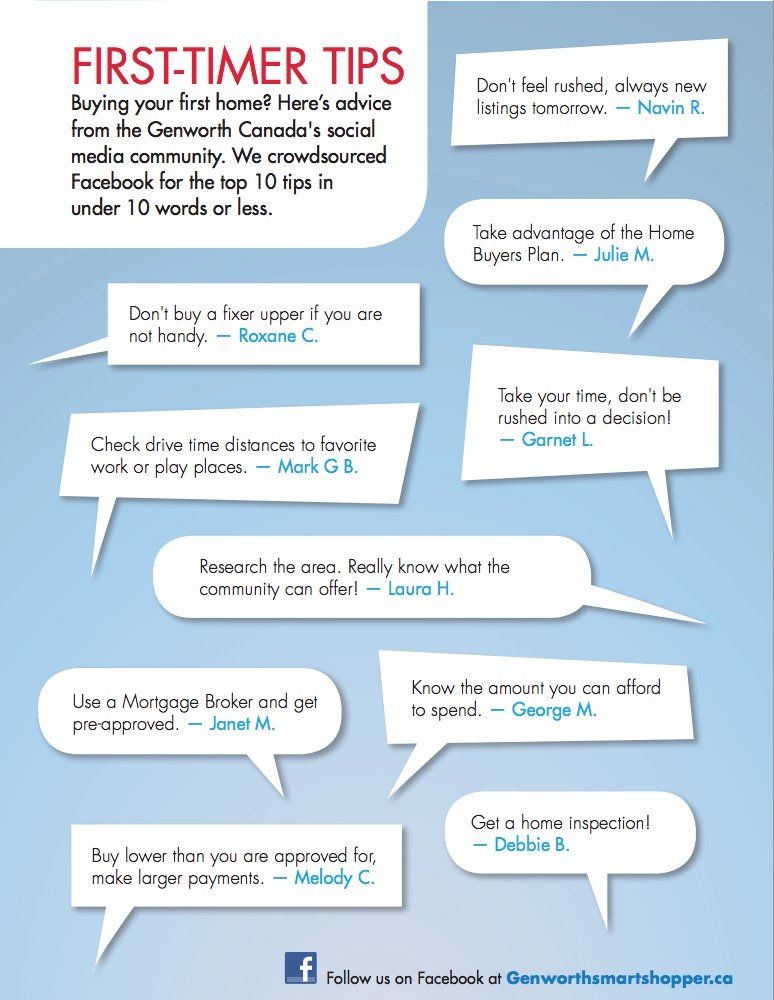

10 Tips for First Time Home Buyers in 10 Words or Less

As part of Genworth’s Homeownership Education Week Seminar, Genworth decided to get social and ask recent first time homebuyers to give simple advice to others looking to purchase their first home. The results were captured and included in the Spring issue of Genworth’s online publication. Below is the Infographic from that publication!

Genworth also published a longer form version of this article on their website. It contains some pretty good advice!

5 Crowdsourced Lessons from First Time Home Buyers

Buying your first home can be a challenge. But luckily you’re not alone. We gathered advice from Genworth Canada’s Facebook page, folks who’ve been there, done that.

Here are the top five tips from the many our first-time homebuyers had to share:

Don’t buy a fixer upper if you are not handy. — Roxane C.

Moving into a fixer-upper is only a great deal if you can do most of the work yourself. It’s more than knowing how to do repairs or being equipped with the necessary tools. It’s the willingness to live in the middle of ongoing projects, and work – every evening – after your day job is done.

Research the area. Really know what the community can offer! — Laura H.

Get to know what a community offers and also where everything is situated. So while you’re checking the quality of nearby schools, check drive-time distances to work and other destinations. Even your dream home becomes less dreamy when you discover you’re a 20-minute drive from a cup o’ coffee.

Don’t feel rushed, always new listings tomorrow. — Navin R.

We all want to move into our first home immediately. Whether it’s love at first sight with a property, or flat-out eagerness to become an actual homeowner, try to resist! There are always new listings tomorrow.

Get a home inspection! — Debbie B.

A home inspection will put your mind at ease that your prospective purchase is in decent shape, establish that the seller has nothing to hide, and will inform you of any future maintenance or required upkeep. No surprises are good!

Take advantage of the Homebuyers Plan. — Julie M.

If you’re uncertain about making the move to homeownership because you’re concerned about having the requisite finances together, the Genworth Canada Homebuyer 95 program provides qualified borrowers with an opportunity to own a home with as little as a 5% down payment.

If you are a looking to buy your first home, but have absolutely no idea where to start, we should probably talk! We would love to walk you through the process and answer any questions you have!

Share

Sign up to to our newsletter to hear weekly updates on market news, timely buyer/seller tips, and up to date rates